If Michael Lewis was indeed embedded with SBF for 6 months, that raises a number of questions:

A) did he see through the Ponzi? B) if so, why didn’t he break the story? C) would it be ethical to stay silent if he knew, in order to gather a more explosive story/book sales? D) or did he actually see SBF as Skywalker vs CZ as Vader?

Media reports seem to point towards D), which would not exactly cast Lewis in a flattering light. Did he too drink the FTX Kool-Aid?

Crisis may ultimately reveal that the supply of Bitcoin is scarcer than it appears.

The tragedy of the current “Crypto” crisis is that Bitcoin is being punished for the sins of SBF — never mind that the demise of FTX does not in any way discredit the value proposition of Bitcoin. On the contrary, FTX was everything Bitcoin is not.

The crisis has triggered a wave of margin calls, liquidations and panic selling, sending the Bitcoin price sharply lower. That is a natural first-order effect, as people question the merits of cryptocurrencies and declare the death of Bitcoin.

There is widespread belief that a cascading crisis will trigger a flood of further Bitcoin liquidations, as exchanges, lenders and funds fail one after another. But how much further can it go?

3AC, Voyager, Celsius and now FTX/Alameda are all in or entering liquidation. But what they all have in common — contrary to what the layperson would intuitively believe about crypto companies — is that they all hold preciously few bitcoins on their balance sheets.

It is staggering that FTX listed 0 bitcoin on its balance sheet, against $1,4 billion of bitcoin liabilities. But, what that obviously means is that there will be no bitcoins to auction off from the ashes of FTX.

3AC was estimated to have around $4 billion worth of assets when it went bankrupt in April — at current market prices it may be half the value or less now.

I don’t know the composition of the 3AC’s remaining assets. But what is sure is that 3AC did not possess the 15,250 bitcoins it owed to Voyager, which in turn sent that firm down:

Pursuant to the 3AC Loan, Voyager agreed to lend 3AC 15,250 Bitcoins and 350 million USDC; 3AC drew down on the entire 3AC Loan. After the Luna crash in 2022, Voyager initially requested partial repayment of the 3AC Loan, and subsequently requested full repayment by June 27, 2022. 3AC did not honor either repayment request. 3AC’s nonpayment, among other things, resulted in Voyager filing its own chapter 11 case in the United States Bankruptcy Court for the Southern District of New York on July 5, 2022.

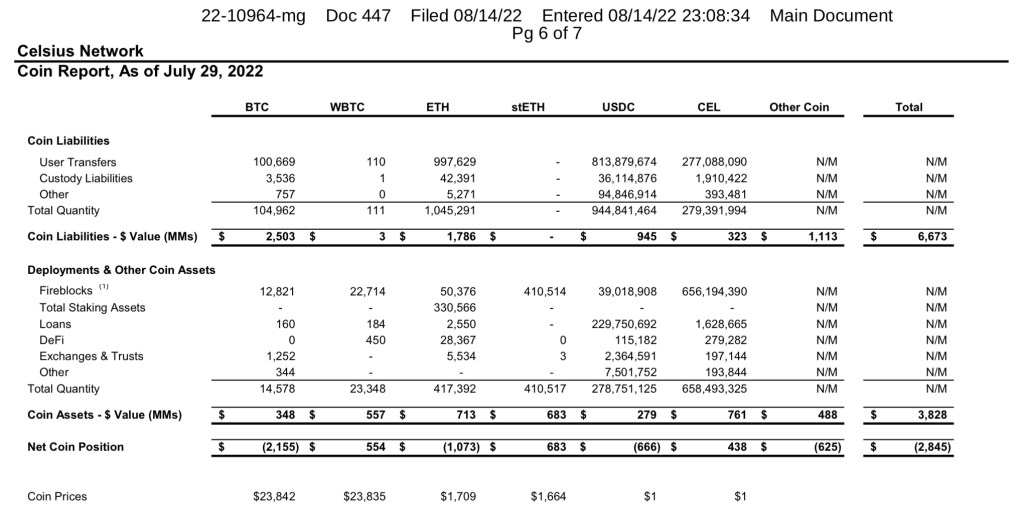

That is quoted from the bankruptcy filing of Celsius, the week after Voyager went down. Celsius’ original filing on July 14th listed a $1,2 billion gap between assets and liabilities. By August that gap had widened to $2,8 billion, as the value of assets fell and liabilities swelled.

A court filing in August showed that Celsius held only 14,578 BTC (~$250m at current prices), (+ 23,348 wrapped bitcoins, for whatever they will be worth), against 104,962 BTC (~$1,75b at current prices) that it owes to clients and creditors. The result of this is of course that people own way less actual bitcoins than they believed they owned.

On Nov. 11th Voyager announced that it is reopening the bidding process for its assets, now that the “$1,4 billion” sale to FTX is of — or $51 million, which was the actual amount of cash to be paid. What will happen with BlockFi, which was also supposed to be taken over by FTX, is also up in the air again. I don’t have the exact figures, but it appears unlikely that any of these companies hold more bitcoins on the asset side than the liability side of their balance sheets.

Of course the crisis may continue to cascade and engulf other players. Crypto.com appears to be next in line for a run on the bank. Crypto.com holds approx. $800 million worth of Bitcoin, according to Nansen, around a third of its total digital coin holdings. Further rounds of forced bitcoin selling can absolutely not be ruled out.

Still, it appears (with provisos of course) that the end result of the domino of falling crypto companies will not be too flood the market with bitcoins, but rather to demonstrate that the supply of actual bitcoins in circulation is much scarcer than the fractional reserve operations of FTX and the other ponzis have given the impression of. That may ultimately turn out to be the silver lining of the crypto crisis.

The Allen Farrington piece on Sequoia’s investment in FTX and hyping of SBF is hilarious.

Moral of the story:

Next time somebody says they don’t read books, don’t make up a mumbo jumbo explanation why that makes the person a next-level genius. Take it instead as confirmation that the person is a fool.

“Wouldn’t someone with IQ points to spare realize that dismissing books — all books — as essentially worthless might rile a writer? Was he playing with me? Is this fun? Is this humor? I’m satisfied with my meta-analysis until I realize that one can always increment the level of strategic play in this sort of game. It’s like poker. Level one is just thinking about how to strengthen your own hand. Level two is thinking about what your opponent’s hand is. Level three is thinking about what your opponent thinks your hand is. And so on. And, since SBF is obviously a genius, I should simply assume that, compared with me, SBF will always be playing at level N+1. Which makes my analysis of the intent behind SBF’s “books are for losers” idea spiral into infinity and crash, like a computer program stuck in a loop.”

On the one hand, even if FTX needs upwards of $8 billion to fill the gaps, which presumably would give the new investors 100% ownership, that would be a lot lower than the $32 billion FTX was valued at earlier this year. On the other hand the business was probably never inherently worth $32 billion, and especially not after what now has transpired.

But it may be too soon to write off FTX entirely yet. One can see a rational for vulture investors to enter the fray.

Cowen also speculates that the market for crypto exchanges might evolve into a natural monopoly over time — with Binance looking like the obvious monopolist following FTX’s demise.

It is also true that a dominant clearinghouse is much easier to regulate, and indeed modern central banks often sprung out of these earlier clearinghouse arrangements. Sooner or later, there is a tendency for the law to intervene and turn the dominant private clearinghouse into part of a more formalized central bank.

A future with Binance as the central bank of crypto? It is possible to imagine, even if it would be very far from Satoshi’s original vision.

I wrote yesterday that CZ and Binance had probably passed the point of no return and could not “backtrack now without inflicting even greater collateral damage on Binance and the cryptocurrency industry in general”.

The further steep decline in the BTC price after the news broke of Binance walking away from the deal, proves that point.

That can only mean that Binance’s DD team found a black hole of unimaginable proportions once they started to inspect FTX’s balance sheet, and must have concluded that the risk to Binance of taking over the toxic waste of FTX was greater than the risk of walking away.

Given that CZ was evidently perfectly aware of the collateral damage his backtracking would inflict on the broader crypto market in this fragile hour — as well as the financial markets in general — that speaks magnitudes about how bad the mess at FTX is.

Only weeks ago Sam Bankman-Fried was hailed as the J.P. Morgan of the cryptosphere, bailing out flailing crypto companies as the industry’s lender of last resort. Now he is the latest Crypto Icarus to have come crashing down to Earth.

SBF’s demise happened at the hands of his rival, Changpeng Zhao or CZ of Binance, who now reigns supreme as the undisputed overlord of the cryptocurrency industry.

While all analysis at this stage is speculative, the attack appears to have been straight out of the Art of War textbook. It will surely be the subject of business school case studies in years to come.

The supreme art of war is to subdue the enemy without fighting.

Sun Tzu

The great showdown started on November 6th when CZ tweeted that Binance would liquidate the entirety of its more than $500 million worth of FTT holdings.

As part of Binance’s exit from FTX equity last year, Binance received roughly $2.1 billion USD equivalent in cash (BUSD and FTT). Due to recent revelations that have came to light, we have decided to liquidate any remaining FTT on our books. 1/4

The radio silence CZ’s thread was met with from the normally high frequency tweeting SBF was deafening.

The response from Alameda CEO, Caroline Ellison, that the hedge fund would happily buy back Binance’s stack of FTT @22$ was probably meant to inspire confidence. Instead it smacked of desperation.

@cz_binance if you're looking to minimize the market impact on your FTT sales, Alameda will happily buy it all from you today at $22!

At this point the game theorist SBF was caught in his very own prisoner’s dilemma with no way out. Which is somewhat ironic given that SBF and FTX had by all accounts already “betrayed” CZ by lobbying against Binance behind their backs, which CZ referenced in one of his follow-up tweets:

Liquidating our FTT is just post-exit risk management, learning from LUNA. We gave support before, but we won't pretend to make love after divorce. We are not against anyone. But we won't support people who lobby against other industry players behind their backs. Onwards.

A political decision SBF may well come to rue now that he no longer has the lordly fortune to realize his political ambitions. He of all people must have known that betrayal does not lead to the Pareto optimal outcome in a prisoner’s dilemma? Or did he really believe he could betray Binance without CZ noticing? Or had he read too many of and started to believe all the magazine pieces hailing him as the crypto world’s infallible wunderkind?

More Madoff than Morgan?

The “recent revelations” in CZ’s tweet referred to the Nov 2nd Coindesk report about Alameda Research, which appeared to show that the majority of the net equity of SBF’s trading firm comprised of FTT and other SBF-associated tokens. The rumour mill went into high gear with questions about Alameda’s solvency.

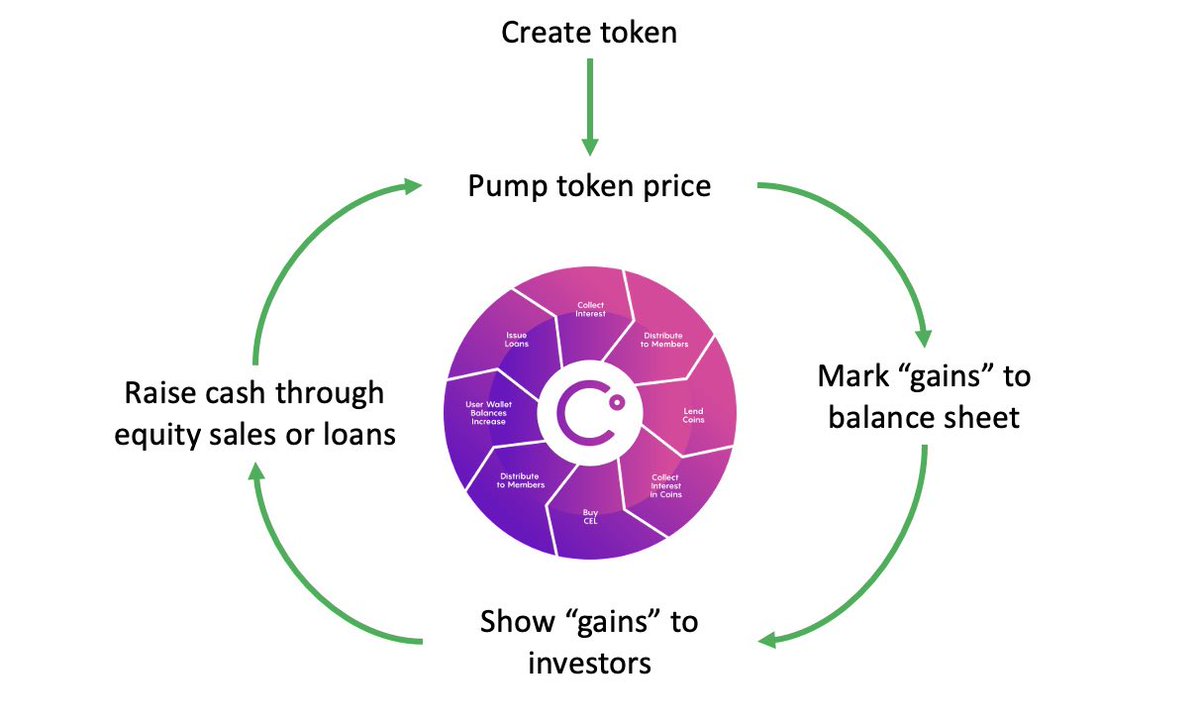

Dirty Bubble Media accused the genius-declared SBF of running precisely the same business model aka ponzi scheme that doomed the crypto lender Celsius Network earlier this year:

Indeed, SBF had raised eyebrows with his cynical description of yield farming schemes on Bloomberg’s Odd Lots podcast back in April. Basically he said that it is little more than black boxes that purport to create money out of thin air. As it turns out it was a fitting description for his own business as well.

It is plausible that CZ was aware of this Achilles heel on Alameda’s balance sheet(?), despite his claims to the contrary.

Having sent out his foreboding tweetstorm all CZ had to do was to sit back and wait for the ensuing bank run on FTX — notwithstanding the collateral damage on the broader cryptocurrency markets.

On Nov 8th SBF was left with no other option than to fold his hand and ask for CZ’s mercy, after client withdrawal requests had clogged up and put FTX in a liquidity squeeze, while the tanking price of the FTT and other SBF-linked tokens had probably rendered Alameda de facto insolvent.

Denouement

The announcement that Binance will acquire FTX was perhaps more shocking than surprising. The deal is naturally subject to all sorts of due diligence. But even if FTX’s business retains zero intrinsic value, CZ has probably passed the point of no return and cannot backtrack now without inflicting even greater collateral damage on Binance and the cryptocurrency industry in general.

Even now questions are being raised if CZ has won a Pyrrhic victory. Has he become the Sun King of crypto at the cost of having shattering the industry in the process? It is a fair question. The price action of Bitcoin and Ether speaks for itself, not to even mention other altcoins.

A sense of despair, even among crypto industry stalwarts, appear to be widespread after recent days’ events. 2022 has seen the demise of many a crypto Demigod. But SBF was somehow believed to be a more noble soul. All the PR, Conversations with Tyler, opinionating on effective altruism and political pontifications painted a picture of a statesmanlike figure. But as it turns out the substance was never quite what the facade of stadium naming rights, celebrity endorsements and Scaramuccian schmoozing gave the impression of.

Healing and Renewal?

One must assume that CZ takes the longer view and believes it is worth cementing his position as the industry leader of the future, at the cost of huge market pain in the present. It is a gamble, but a reasonable one.

The risks are numerous:

The whole crypto space is likely to face intense regulatory scrutiny in light of the recent shitstorm — will CZ partner with the regulators like SBF did? Or more likely will he continue to take a more two-faced approach?

Will existing users even bother to hang around in the crypto hellhole after this Annus horribilis?

What will attract new users to this hornet nest casino which almost makes the Turkish lira, the Argentine peso and the Lebanese pound look trustworthy in comparison, (though that may be to stretch it).

Crypto was supposed to be trustless. But in a good way, not like this, where it turns out nobody, not even the most well-reputed exchanges can be trusted.

And specific to the deal itself; will Binance be immune to contagion from the toxic company it is acquiring? Or can FTX create a black hole in Binance’s balance sheet which will bring down it as well? Or will it prove too difficult to get the deal completed?

Or will the deal go through and make Binance an overly dominant player in the crypto space?

Only time will tell. For now it all looks like doom and gloom. For all the pain and misery in the crypto space this year, the current market mayhem is a necessary cleansing process to root out all the bad weeds that have permeated the industry to its core. Whether CZ is the redeeming angel is another matter altogether. But perhaps like in the Twilight of the Gods, that once all the burning and flooding is done, it will lead to the renewal of the [crypto] world?

One of the most long-awaited events in the cryptocurrency space appears to finally actually be happening: Ethereum’s transition from Proof-of-Work (PoW) to Proof-of-Stake (PoS).

The transformation of the second largest blockchain has long been shrouded in fear, uncertainty and doubt. The onset of a new crypto winter led many to believe that the change would be postponed yet again or not happen at all, in the face of insurmountable complexity and civil war within the Ethereum community.

That still cannot be ruled out. But with market sentiment recently being at rock bottom, much more attention has been paid to all the possible ways the Merge could derail, rather than the fact that the process has been moving forward.

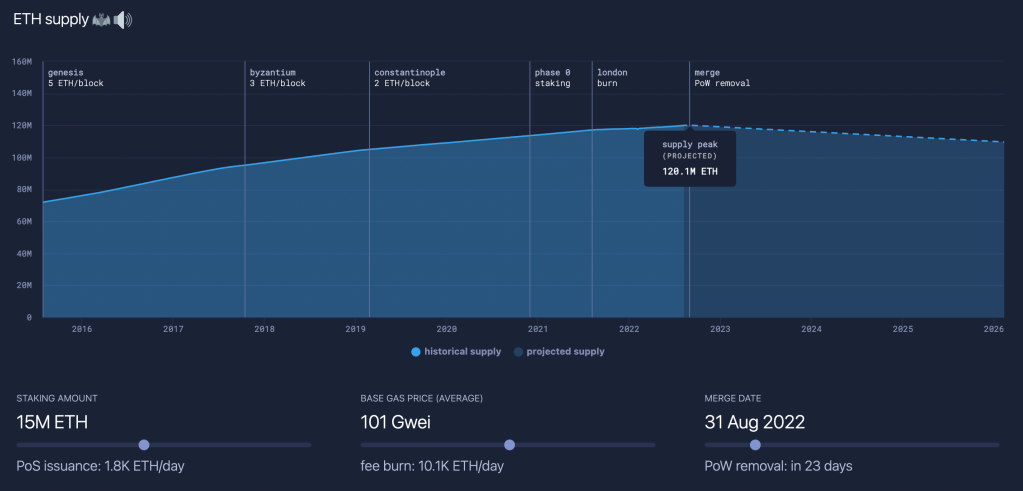

The third and final rehearsal before the Mainnet Merge is taking place this week, when the Goerli testnet transitions to PoS, expected to be completed by August 12th. Provided that the testnet merge goes according to plan an announcement of the time schedule for the Mainnet Merge is likely to follow.

The Mainnet Merge will see the legacy (PoW) Ethereum blockchain is being merged with a special-purpose (PoS) blockchain called the Beacon Chain, which launched on December 1st, 2020. (Bankless has compiled an informative list of FAQs surrounding the Merge here and another good primer can be read here.)

90% lower ETH issuance

The Merge, provided it succeeds, will lead to a ~90% reduction in ETH issuance. Money supply growth will reduce from ~4% per year to close to zero. The effects of the Merge on ETH money supply can be simulated here. The overall supply of ETH in circulation will peak around the Merge and is predicted to decline going forward as the amount of ETH being burnt outstrips the amount of ETH being issued.

The Merge has been likened to a “Triple halving”, in Bitcoin parlance, because the deflationary impact of the change to PoS is roughly equivalent to the effect of three Bitcoin halvings (which of course only happens once every fourth year, with the next one on track in 2024).

With annual ETH issuance being reduced by approx. 5 million ETH, that translates to approx. $8,5b at current prices (~1.700USD/ETH). Considering that most new ETH issuance have tended to be sold directly in the market by miners, that is a lot of selling pressure that will disappear going forward after the Merge.

~99.95% less energy use

Post-Merge, Ethereum will also use ~99.95% less energy than it currently does.

Whether changing to PoS represents an improvement from PoW is a separate debate. But the change to PoS pre-empts any criticism of Ethereum for heavy energy use. If that will lead to increased adoption/investment from actors that previously have had ESG concerns remains to be seen, but it is definitely a possibility given how sticky (fair or unfair) the energy critique has been.

Miner Revolt?

So will the Merge now actually happen? Or will it be delayed yet again?

In his latest essay where he outlines why he is “max bidding” ETH Arthur Hayes makes a logical deduction why he believes the Merge now is for real. Because the one group that is both the best informed and that stand to lose the most from the Merge, namely the Ethereum miners, is turning increasingly vocal about and mobilising against the Merge.

Just like Bitcoin miners Ethereum miners have been generating revenue by solving computationally difficult puzzles to produce blocks of transactions. With the transition to PoS the miners will be rendered out of business. There are few if any other blockchains with the size and scale of Ethereum that the miners can allocate their resources to instead. Naturally they are not happy. Some have indicated that they will turn to supporting Ethereum Classic, that hard-forked from Ethereum in 2016.

Another very possible scenario is that the Merge will lead to another hard-fork and the creation of a PoW Ethereum blockchain that will continue to run in parallel with the main PoS chain.

Whereas the miners stand to lose, validators stand to generate attractive returns from staking ETH under the new PoS mechanism. If the Merge happened today, validators could expect to earn a total of ~8–12% APR, although yields are likely to be brought down as the demand for staking ETH increases.

The yield-earning potential from ETH staking (without the type of crazy credit risk that recently got many speculators in various DeFi yield farming schemes severly burnt) is a potential game changer, as it significantly increases the attractiveness of Ethereum as a financial asset.

Price volatility will in all likelihood continue to be a feature, but for investors that in any case would be holding ETH, the ability to pocket yields is a big added advantage.

While Ethereum remains down approximately 2/3 from the November ATH, it has doubled from the June bottoms below $1.000, as the sentiment has tentatively improved.

There is of course still a chance that the Ethereum Merge could turn into an unmitigated disaster, which in case would freeze the whole Cryptosphere in a deep winter like the White Witch of Narnia. But for the moment it does actually look like the Merge will at long last take place and turn Ethereum into an energy efficient, environmentally friendly Blockchain, that will further distinguish it from its big brother Bitcoin.

10-15 years ago Gillian Tett was a fine journalist, offering fresh and insightful commentary on the tubing of financial markets. For example her book, “Fool’s Gold” – on the origins of the CDO debacle – was great.

That is quite some time ago. Since then Tett has been effectively co-opted by the liberal Manhattan establishment, and rarely (if ever) has anything interesting to offer anymore.

To be fair, Tett is more crypto-curious than the FT’s otherwise categorically negative stance towards the space. But her latest piece is somewhat confused.

The entire cryptocurrency complex, Bitcoin included, has no doubt taken a heavy beating this year. And SBF has offered credit lines to crumbling competitors like a latter-day J.P. Morgan. But. No government bailouts have been required. And whilst the Bitcoin price has plummeted, the network is stronger than ever.

So, why the implosion of the “terra and luna stable coins”, as Tett imprecisely describes, would be “distinctly embarrassing for crypto evangelists”, is far from clear, when in fact the loudest warnings against Do Kwon’s un-stable/Ponzi coin scheme came from within the crypto community.

I.e. Tett is guilty of equalling crypto with Bitcoin.

It is understandable that the recent turmoil has put many people off cryptocurrencies in general, at least in the short term.

But in the longer term the collapse of UST, Luna, 3AC, Celsius, etc, and articles like this one from Tett will serve to underline that:

Crypto ≠ Bitcoin

Gillian Tett needs to dig deeper down the rabbit hole next time.

Most Bitcoin books are bad. Many fall in the category of overzealous Bitcoin Maximalist tracts, reading more like religious scripture than factually enlightening non-fiction.

The “Blocksize Wars” is of a different breed. The title admittedly sounds boring. And the subtitle – “the battle for control over Bitcoin’s protocol rules” – even more so.

That is precisely why you should read it. Jonathan Bier chronicles what on the face of it looked like a quite narrow technical disagreement within the Bitcoin community, but which revealed a deep underlying philosophical schism, with two competing visions for what Bitcoin should be. This was Bitcoin’s equivalent of Christianity’s split between Catholicism and Protestantism or the Shia-Sunni divide within Islam.

The two diverging factions that went to war between 2015 – 2017 became known as the small blockers and the big blockers. The former being textualists who wanted to stick to Bitcoin’s pseudonymous founder Satoshi Nakamoto’s original idea of how the cryptocurrency should work, whereas the latter faction preferred a more constructionist approach allowing greater scope for amending and adapting the Bitcoin protocol like a living constitution to new circumstances as time goes by.

The primary point of contention was Bitcoin’s blocksize limit, i.e. the amount of data available in each Bitcoin block. Whereas the big blockers deemed it necessary to progressively increase the blocksize limit in order to facilitate faster and cheaper transactions on the Bitcoin blockchain, the small blockers wanted to keep the original 1MB blocksize limit, (which was actually not included in the code at the time of Bitcoin’s initial release in January 2009 but was introduced by Satoshi a year and a half after in the summer of 2010).

As Bier recounts at stake was not only the technical matter of the blocksize limit, but the fundamental question of how Bitcoin’s protocol rules could be modified, and by whom. Does power over Bitcoin lie with miners or with the ultimate end users? And what time preference should Bitcoin be dictated by? Should Bitcoin be like a tech startup and prioritise gaining market share in the short term: or was it a long-term project, a new global money, that should think decades ahead when making decisions? Should its aim be to offer a fast and cheap payments network to compete with the likes of Visa and Mastercard? Or should Bitcoin’s rather aim to be a form of digital gold, that is used more as a store of value than for small daily transactions?

The plot has arguably gained renewed relevance in light of Tesla founder Elon Musk’s emergence in the cryptosphere as a late-coming big blocker.

The reason why Musk has turned his attention to Dogecoin is because his side of the argument lost. The small blockers won the war.

Why? Did Musk miss something?

At least the arguments Musk have recently been making about Bitcoin scalability sounds like a re-enactment of the [losing] arguments the big blockers made during the Blocksize war.

I will not provide a full account of the war. For that, read the book. But for the briefest of summaries: The opening shots were fired in August 2015 when ur-Bitcoiners Mike Hearn and Gavin Andresen threw their weight behind a new, incompatible version of Bitcoin, known as Bitcoin XT, that would increase the blocksize limit to 8MB and progressively double it every two years until 2036.

According to the big blockers such an increase was necessary for Bitcoin to be able to process more transactions cheaper and faster, which in their world view was a prerequisite for Bitcoin to offer a viable use case and gain mass adoption.

The scheduled implementation of this proposal was five months later in January 2016, and required a vote from the Bitcoin miners, with 75 percent support set as the threshold for activation.

What made the proposal instantly controversial was that it incompatible with the existing Bitcoin network, and thereby would require anyone running a Bitcoin node – (the decentralised network of computers that validate transactions and store the entire blockchain) – to upgrade their software.

If the upgrade had gone ahead it would have constituted what is referred to as a hard fork, i.e. a point where the blockchain can bifurcate and potentially split into two separate coins. To cut a long story short, Bitcoin XT and its successor proposals failed, but a hard fork splitting Bitcoin in two was eventually what happened with the birth of Bitcoin Cash on August 1st 2017. (And then in November 2018 Bitcoin SV split off from that chain again).

So why did the small blockers win the war? And what did it mean?

Interestingly they did win despite being the presumptive underdogs. Gavin Andresen was the closest thing to Satoshi Nakamoto’s heir apparent, and did not hide his pretensions to the throne. Almost all the big crypto corporations, Coinbase notably, supported the big blockers.

But as in Afghanistan an apparent underdog may very well conquer a materially superior enemy if it has strategic patience and more nimble tactics. Having a better understanding of the battlefield also helps.

The main philosophical differences between the small blockers and the big blockers can be summarised more or less as in the below table.

Small Blockers:

Large Blockers:

Long term

Short term

System resilience

User experience

Sustainability

Growth

Theoretical / Scientific

Pragmatic

Cryptography nerds

Business-minded

Ultra decentralisation

Mild Decentralisation

To over-simplify: the nerds beat the suits.

For uninitiated but crypto-curious readers The Blocksize Wars might be as good a primer as any. You have to jump down the rabbit hole from somewhere. Bier provides a very well detailed account of all the battles of the war, with all the technical intricacies at stake, which are interesting in and of themselves, particularly for more initiated readers. Yet he manages to convey the essence of the opposing world views in the overarching philosophical conflict in terms that are perfectly clear even to the lay reader.

The fact that Bitcoin is a decentralised network with an unknown founder makes it stand out remarkably from other emerging technologies in recent times, that have mostly fallen under the control of centralised oligopolies, the tech giants of Silicon Valley and their autocratic founders coming first to mind. As venture capitalist Marc Andreessen said in a recent interview the immaculate conception of Bitcoin from the depths of the Internet and the fact that its creator remains shrouded in mystery “is one of the most amazing things I have seen my entire life.”

What Bier’s book drives home very clearly is how the decentralised nature of Bitcoin limits the power of any one actor. For example Gavin Andresen thought he could use his authority as Satoshi’s heir to force through his vision for Bitcoin. But his hubris was quickly humbled. Likewise the “Fake Satoshi”, Craig Wright. As well as the Bitcoin miners.

At the outset of the Blocksize war the balance of power was assumed to lie with the miners. But what the war revealed was that while the miners play a vital role in running and securing the Bitcoin network, they are far from all-powerful and cannot force through change without the support of nodes and end users.

The most feared known unknown for Bitcoin is a so-called 51% attack, whereby a constellation of malevolent miners gains control of more than 51% of the network and can manipulate the Blockchain in order to potentially double-spend coins.

However, after reading Bier’s book you do start to question how real the risk of a 51% attack really is for Bitcoin, (Bitcoin SV appears to have suffered one recently). It is questionable how much rogue miners would be able to gain from committing a hostile attack without ipso facto negating the theoretical gains from the attack.

Without consensus the attackers may not be able to get very far. Even if the attackers should succeed in sustaining a malignant chain with a bigger number of blocks in it than the main chain for some time, it is questionable if they will be able to force acceptance of this chain on the rest of the community. The Blocksize war proved that the majority chain will not necessarily be considered the “legitimate” chain, solely on the basis of being the majority chain. In all likelihood the price of “Bitcoin” on the illegitimate chain would plummet, thus undermining the profits of the attackers and dis-incentivising miners from working on the chain. Even a successful 51% attack could thus easily prove to be a Pyrrhic victory at most, (as demonstrated in the somewhat similar case of Justin Sun’s failed attack on STEEM, which Vitalik Buterin has written interestingly in his post on Legitimacy).

It has become a cliche that bitcoiners are “in it for the tech”, not the money. The fact of the matter however is that the money talks. Technology follows the money. The two are inseparable. Technology will gravitate toward the most valuable blockchain. Value in turn depend on trust and legitimacy. If Bitcoin does not have trust and legitimacy it will not have value either. The reason why Bitcoin does have trust and legitimacy is because it is consensus-based. It is the monetary democracy. Attackers can in theory succeed in taking over the network, but not without dooming it and themselves. The likelihood that there exist an entity that possesses both a) the technological sophistication and resources to master a 51% attack, and b) the monetary ignorance to actually carry out such a self-defeating attack, must therefore be considered to be quite small, though it cannot be ruled out completely.

The monster of Stagflation is finally rearing its ugly head again, after more than a decade of massive money printing by central banks.

The central bankers thought “Quantitative Easing” would boost economic growth without stoking inflation. But ultimately this unprecedented monetary experiment may end with spiralling inflation and stagnating growth – with Milton Friedman lecturing from heaven that “inflation is always and everywhere a monetary phenomenon”.

Ironically, Bitcoin, which was created precisely as an antidote to inflationary monetary policies, also plunged after the inflation report.

The Bitcoin dump accelerated further after Elon Musk tweeted that Tesla will not be accepting Bitcoin payment for Teslas after all, (which do raise some interesting questions about the company’s due diligence practices, but never mind).

On the face of it the tweet is bearish for the Bitcoin price, which duly tanked as low as $45.000.

But, how many people would have exchanged Bitcoin for Teslas anyway? Probably not many. And those few would already be holders of Bitcoin. Nobody would exchange fiat currency for Bitcoin for the purpose of buying a Tesla. Ergo, the initial Tesla announcement of Bitcoin acceptance, though much hyped at the time, did not imply any new marginal demand for Bitcoin. If anything, Musk’ statement may inadvertently lead to less demand for Teslas from Bitcoiners.

Likewise, Wednesday’s reversal statement from Musk should not have any implications for Bitcoin demand. Despite dressing up the announcement in environmentally conscious lingo the bottom line is that Tesla will keep hodling Bitcoin. Mr Musk is a mercurial character and it is not easy to know if he has a bigger plan or is just acting ad hoc, but in this case it may very well be the latter.

In any case Mr Musk’s tweet sowed much fear, uncertainty and doubt. But in a world where consumer prices are accelerating ominously, Tesla’s self-appointed techno-king is presenting late-coming hedge fund managers and the Michael Saylors of the world with an opportunity to pick up Bitcoin on the cheap. As I write this the price is already back above $50.000 again, (Caveat Emptor)