On the one hand, even if FTX needs upwards of $8 billion to fill the gaps, which presumably would give the new investors 100% ownership, that would be a lot lower than the $32 billion FTX was valued at earlier this year. On the other hand the business was probably never inherently worth $32 billion, and especially not after what now has transpired.

But it may be too soon to write off FTX entirely yet. One can see a rational for vulture investors to enter the fray.

Cowen also speculates that the market for crypto exchanges might evolve into a natural monopoly over time — with Binance looking like the obvious monopolist following FTX’s demise.

It is also true that a dominant clearinghouse is much easier to regulate, and indeed modern central banks often sprung out of these earlier clearinghouse arrangements. Sooner or later, there is a tendency for the law to intervene and turn the dominant private clearinghouse into part of a more formalized central bank.

A future with Binance as the central bank of crypto? It is possible to imagine, even if it would be very far from Satoshi’s original vision.

I wrote yesterday that CZ and Binance had probably passed the point of no return and could not “backtrack now without inflicting even greater collateral damage on Binance and the cryptocurrency industry in general”.

The further steep decline in the BTC price after the news broke of Binance walking away from the deal, proves that point.

That can only mean that Binance’s DD team found a black hole of unimaginable proportions once they started to inspect FTX’s balance sheet, and must have concluded that the risk to Binance of taking over the toxic waste of FTX was greater than the risk of walking away.

Given that CZ was evidently perfectly aware of the collateral damage his backtracking would inflict on the broader crypto market in this fragile hour — as well as the financial markets in general — that speaks magnitudes about how bad the mess at FTX is.

Only weeks ago Sam Bankman-Fried was hailed as the J.P. Morgan of the cryptosphere, bailing out flailing crypto companies as the industry’s lender of last resort. Now he is the latest Crypto Icarus to have come crashing down to Earth.

SBF’s demise happened at the hands of his rival, Changpeng Zhao or CZ of Binance, who now reigns supreme as the undisputed overlord of the cryptocurrency industry.

While all analysis at this stage is speculative, the attack appears to have been straight out of the Art of War textbook. It will surely be the subject of business school case studies in years to come.

The supreme art of war is to subdue the enemy without fighting.

Sun Tzu

The great showdown started on November 6th when CZ tweeted that Binance would liquidate the entirety of its more than $500 million worth of FTT holdings.

As part of Binance’s exit from FTX equity last year, Binance received roughly $2.1 billion USD equivalent in cash (BUSD and FTT). Due to recent revelations that have came to light, we have decided to liquidate any remaining FTT on our books. 1/4

The radio silence CZ’s thread was met with from the normally high frequency tweeting SBF was deafening.

The response from Alameda CEO, Caroline Ellison, that the hedge fund would happily buy back Binance’s stack of FTT @22$ was probably meant to inspire confidence. Instead it smacked of desperation.

@cz_binance if you're looking to minimize the market impact on your FTT sales, Alameda will happily buy it all from you today at $22!

At this point the game theorist SBF was caught in his very own prisoner’s dilemma with no way out. Which is somewhat ironic given that SBF and FTX had by all accounts already “betrayed” CZ by lobbying against Binance behind their backs, which CZ referenced in one of his follow-up tweets:

Liquidating our FTT is just post-exit risk management, learning from LUNA. We gave support before, but we won't pretend to make love after divorce. We are not against anyone. But we won't support people who lobby against other industry players behind their backs. Onwards.

A political decision SBF may well come to rue now that he no longer has the lordly fortune to realize his political ambitions. He of all people must have known that betrayal does not lead to the Pareto optimal outcome in a prisoner’s dilemma? Or did he really believe he could betray Binance without CZ noticing? Or had he read too many of and started to believe all the magazine pieces hailing him as the crypto world’s infallible wunderkind?

More Madoff than Morgan?

The “recent revelations” in CZ’s tweet referred to the Nov 2nd Coindesk report about Alameda Research, which appeared to show that the majority of the net equity of SBF’s trading firm comprised of FTT and other SBF-associated tokens. The rumour mill went into high gear with questions about Alameda’s solvency.

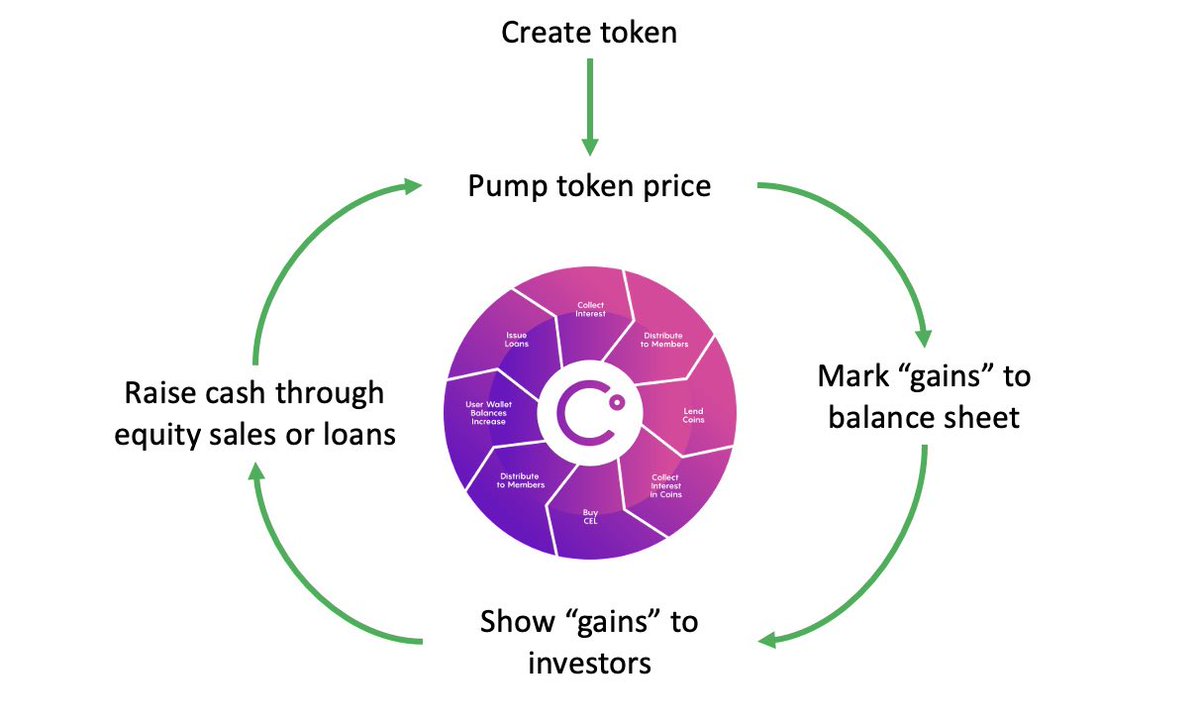

Dirty Bubble Media accused the genius-declared SBF of running precisely the same business model aka ponzi scheme that doomed the crypto lender Celsius Network earlier this year:

Indeed, SBF had raised eyebrows with his cynical description of yield farming schemes on Bloomberg’s Odd Lots podcast back in April. Basically he said that it is little more than black boxes that purport to create money out of thin air. As it turns out it was a fitting description for his own business as well.

It is plausible that CZ was aware of this Achilles heel on Alameda’s balance sheet(?), despite his claims to the contrary.

Having sent out his foreboding tweetstorm all CZ had to do was to sit back and wait for the ensuing bank run on FTX — notwithstanding the collateral damage on the broader cryptocurrency markets.

On Nov 8th SBF was left with no other option than to fold his hand and ask for CZ’s mercy, after client withdrawal requests had clogged up and put FTX in a liquidity squeeze, while the tanking price of the FTT and other SBF-linked tokens had probably rendered Alameda de facto insolvent.

Denouement

The announcement that Binance will acquire FTX was perhaps more shocking than surprising. The deal is naturally subject to all sorts of due diligence. But even if FTX’s business retains zero intrinsic value, CZ has probably passed the point of no return and cannot backtrack now without inflicting even greater collateral damage on Binance and the cryptocurrency industry in general.

Even now questions are being raised if CZ has won a Pyrrhic victory. Has he become the Sun King of crypto at the cost of having shattering the industry in the process? It is a fair question. The price action of Bitcoin and Ether speaks for itself, not to even mention other altcoins.

A sense of despair, even among crypto industry stalwarts, appear to be widespread after recent days’ events. 2022 has seen the demise of many a crypto Demigod. But SBF was somehow believed to be a more noble soul. All the PR, Conversations with Tyler, opinionating on effective altruism and political pontifications painted a picture of a statesmanlike figure. But as it turns out the substance was never quite what the facade of stadium naming rights, celebrity endorsements and Scaramuccian schmoozing gave the impression of.

Healing and Renewal?

One must assume that CZ takes the longer view and believes it is worth cementing his position as the industry leader of the future, at the cost of huge market pain in the present. It is a gamble, but a reasonable one.

The risks are numerous:

The whole crypto space is likely to face intense regulatory scrutiny in light of the recent shitstorm — will CZ partner with the regulators like SBF did? Or more likely will he continue to take a more two-faced approach?

Will existing users even bother to hang around in the crypto hellhole after this Annus horribilis?

What will attract new users to this hornet nest casino which almost makes the Turkish lira, the Argentine peso and the Lebanese pound look trustworthy in comparison, (though that may be to stretch it).

Crypto was supposed to be trustless. But in a good way, not like this, where it turns out nobody, not even the most well-reputed exchanges can be trusted.

And specific to the deal itself; will Binance be immune to contagion from the toxic company it is acquiring? Or can FTX create a black hole in Binance’s balance sheet which will bring down it as well? Or will it prove too difficult to get the deal completed?

Or will the deal go through and make Binance an overly dominant player in the crypto space?

Only time will tell. For now it all looks like doom and gloom. For all the pain and misery in the crypto space this year, the current market mayhem is a necessary cleansing process to root out all the bad weeds that have permeated the industry to its core. Whether CZ is the redeeming angel is another matter altogether. But perhaps like in the Twilight of the Gods, that once all the burning and flooding is done, it will lead to the renewal of the [crypto] world?

One of the most long-awaited events in the cryptocurrency space appears to finally actually be happening: Ethereum’s transition from Proof-of-Work (PoW) to Proof-of-Stake (PoS).

The transformation of the second largest blockchain has long been shrouded in fear, uncertainty and doubt. The onset of a new crypto winter led many to believe that the change would be postponed yet again or not happen at all, in the face of insurmountable complexity and civil war within the Ethereum community.

That still cannot be ruled out. But with market sentiment recently being at rock bottom, much more attention has been paid to all the possible ways the Merge could derail, rather than the fact that the process has been moving forward.

The third and final rehearsal before the Mainnet Merge is taking place this week, when the Goerli testnet transitions to PoS, expected to be completed by August 12th. Provided that the testnet merge goes according to plan an announcement of the time schedule for the Mainnet Merge is likely to follow.

The Mainnet Merge will see the legacy (PoW) Ethereum blockchain is being merged with a special-purpose (PoS) blockchain called the Beacon Chain, which launched on December 1st, 2020. (Bankless has compiled an informative list of FAQs surrounding the Merge here and another good primer can be read here.)

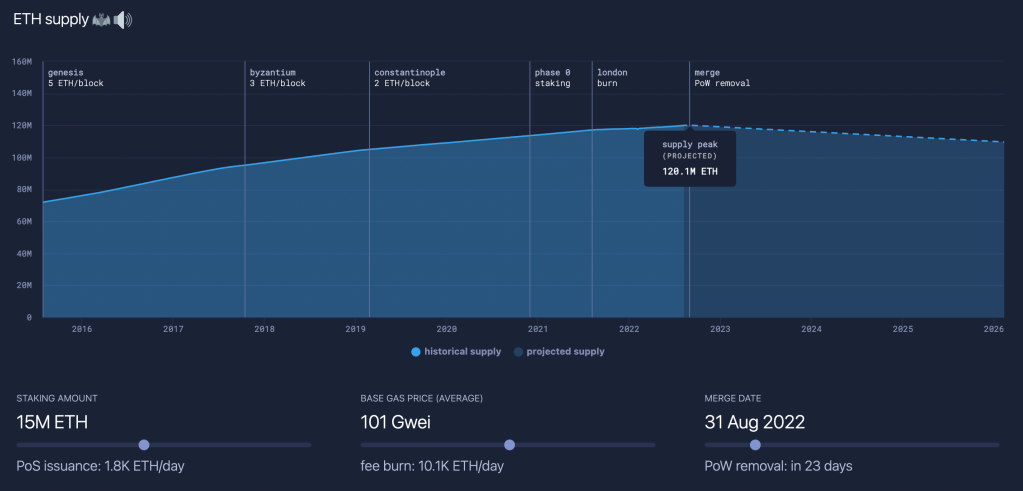

90% lower ETH issuance

The Merge, provided it succeeds, will lead to a ~90% reduction in ETH issuance. Money supply growth will reduce from ~4% per year to close to zero. The effects of the Merge on ETH money supply can be simulated here. The overall supply of ETH in circulation will peak around the Merge and is predicted to decline going forward as the amount of ETH being burnt outstrips the amount of ETH being issued.

The Merge has been likened to a “Triple halving”, in Bitcoin parlance, because the deflationary impact of the change to PoS is roughly equivalent to the effect of three Bitcoin halvings (which of course only happens once every fourth year, with the next one on track in 2024).

With annual ETH issuance being reduced by approx. 5 million ETH, that translates to approx. $8,5b at current prices (~1.700USD/ETH). Considering that most new ETH issuance have tended to be sold directly in the market by miners, that is a lot of selling pressure that will disappear going forward after the Merge.

~99.95% less energy use

Post-Merge, Ethereum will also use ~99.95% less energy than it currently does.

Whether changing to PoS represents an improvement from PoW is a separate debate. But the change to PoS pre-empts any criticism of Ethereum for heavy energy use. If that will lead to increased adoption/investment from actors that previously have had ESG concerns remains to be seen, but it is definitely a possibility given how sticky (fair or unfair) the energy critique has been.

Miner Revolt?

So will the Merge now actually happen? Or will it be delayed yet again?

In his latest essay where he outlines why he is “max bidding” ETH Arthur Hayes makes a logical deduction why he believes the Merge now is for real. Because the one group that is both the best informed and that stand to lose the most from the Merge, namely the Ethereum miners, is turning increasingly vocal about and mobilising against the Merge.

Just like Bitcoin miners Ethereum miners have been generating revenue by solving computationally difficult puzzles to produce blocks of transactions. With the transition to PoS the miners will be rendered out of business. There are few if any other blockchains with the size and scale of Ethereum that the miners can allocate their resources to instead. Naturally they are not happy. Some have indicated that they will turn to supporting Ethereum Classic, that hard-forked from Ethereum in 2016.

Another very possible scenario is that the Merge will lead to another hard-fork and the creation of a PoW Ethereum blockchain that will continue to run in parallel with the main PoS chain.

Whereas the miners stand to lose, validators stand to generate attractive returns from staking ETH under the new PoS mechanism. If the Merge happened today, validators could expect to earn a total of ~8–12% APR, although yields are likely to be brought down as the demand for staking ETH increases.

The yield-earning potential from ETH staking (without the type of crazy credit risk that recently got many speculators in various DeFi yield farming schemes severly burnt) is a potential game changer, as it significantly increases the attractiveness of Ethereum as a financial asset.

Price volatility will in all likelihood continue to be a feature, but for investors that in any case would be holding ETH, the ability to pocket yields is a big added advantage.

While Ethereum remains down approximately 2/3 from the November ATH, it has doubled from the June bottoms below $1.000, as the sentiment has tentatively improved.

There is of course still a chance that the Ethereum Merge could turn into an unmitigated disaster, which in case would freeze the whole Cryptosphere in a deep winter like the White Witch of Narnia. But for the moment it does actually look like the Merge will at long last take place and turn Ethereum into an energy efficient, environmentally friendly Blockchain, that will further distinguish it from its big brother Bitcoin.

10-15 years ago Gillian Tett was a fine journalist, offering fresh and insightful commentary on the tubing of financial markets. For example her book, “Fool’s Gold” – on the origins of the CDO debacle – was great.

That is quite some time ago. Since then Tett has been effectively co-opted by the liberal Manhattan establishment, and rarely (if ever) has anything interesting to offer anymore.

To be fair, Tett is more crypto-curious than the FT’s otherwise categorically negative stance towards the space. But her latest piece is somewhat confused.

The entire cryptocurrency complex, Bitcoin included, has no doubt taken a heavy beating this year. And SBF has offered credit lines to crumbling competitors like a latter-day J.P. Morgan. But. No government bailouts have been required. And whilst the Bitcoin price has plummeted, the network is stronger than ever.

So, why the implosion of the “terra and luna stable coins”, as Tett imprecisely describes, would be “distinctly embarrassing for crypto evangelists”, is far from clear, when in fact the loudest warnings against Do Kwon’s un-stable/Ponzi coin scheme came from within the crypto community.

I.e. Tett is guilty of equalling crypto with Bitcoin.

It is understandable that the recent turmoil has put many people off cryptocurrencies in general, at least in the short term.

But in the longer term the collapse of UST, Luna, 3AC, Celsius, etc, and articles like this one from Tett will serve to underline that:

Crypto ≠ Bitcoin

Gillian Tett needs to dig deeper down the rabbit hole next time.

Crypto may turn out to be far more useful to those looking to move in the open, rather than in the shadows. On February 26th the official Ukrainian Twitter account published digital-wallet addresses through which it is accepting bitcoin, ethereum and other tokens. Nearly $100m-worth of tokens has since been donated. Much of this is being spent on things like bulletproof vests and night-vision goggles, according to Alex Bornyakov, Ukraine’s deputy minister for digital transformation. In extreme events, where it is helpful to shrink the time that elapses between someone deciding to make a donation and that money being put to work, crypto has an obvious advantage. Tokens can be sent to another wallet in seconds, whereas international bank transfers can take days.

All this makes for an interesting transition for crypto. The conflict in Ukraine has brought into focus the financial-crime risks it poses, but also the advantages of speed and ease of transfer it offers over fiat currency—which could help during or after other types of extreme, time-sensitive events too, such as natural disasters. The war makes it clear that there are serious uses for crypto, but that it can expect to be policed more seriously, too.